F&M Bank offices will close at 2:00 PM on Wednesday, December 31 for New Year’s Eve and will be closed Thursday, January 1 for New Year’s Day. Normal business hours will resume Friday, January 2. F&M Mobile & Online Banking is available 24/7.

F&M Bank offices will close at 2:00 PM on Wednesday, December 31 for New Year’s Eve and will be closed Thursday, January 1 for New Year’s Day. Normal business hours will resume Friday, January 2. F&M Mobile & Online Banking is available 24/7.

F & M Bank Corp. Announces Earnings

F & M Bank Corp. (OTCQX:FMBM), parent company of Farmers & Merchants Bank, announces its financial results for the fourth quarter and year ended December 31, 2019.

Selected highlights for the quarter and year to date include:

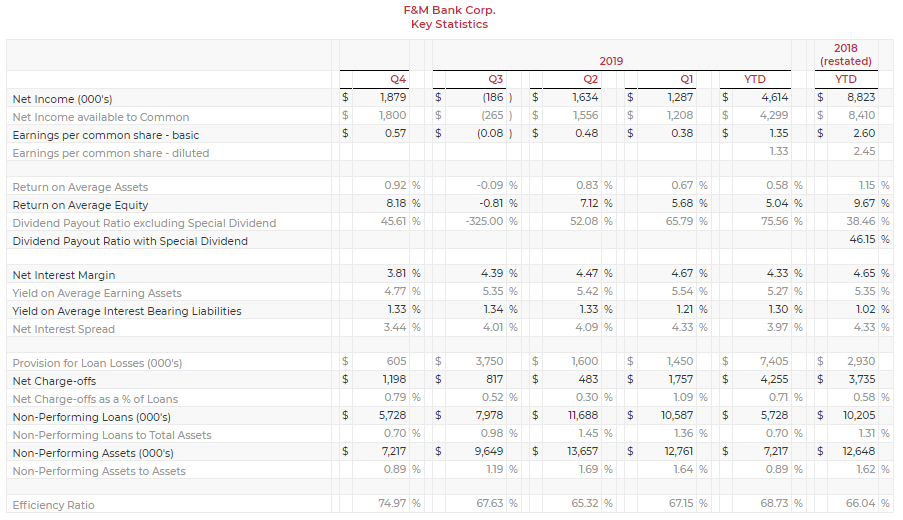

- Net income of $1.9 million and $4.6 million, respectively;

- Non-performing assets decreased $2.43 million during the fourth quarter and $5.43 million year to date;

- Net interest margin 3.81% and 4.33%. respectively;

- Total deposits increased $23.3 million and $50.4 million, respectively for the quarter and year to date.

Mark Hanna, President, commented, “We are pleased to announce fourth quarter and year-to-date earnings of $1.9 million and $4.6 million, respectively. Although these results are lower than prior year, we made great progress in positioning F&M Bank for continued success by substantially reducing our Non-performing assets and growing Core deposit relationships. It is important to note that Fourth Quarter earnings were reduced by several non-recurring items related to dealer deferred cost amortization, pension costs and severance benefits. Our margin decreased as a result of lower loan balances due primarily to sales of indirect dealer loans which occurred during the second half of the year and unrecognized dealer loan costs. Our provision for loan losses increased in 2019 due to higher levels of substandard loans and identification of problem credits. We feel the allowance for loan losses reflects the current risk in our loan portfolio. As we push into 2020, we feel that we are well positioned to leverage our surplus liquidity with organic loan growth and continued improvement in reducing our funding costs.

Hanna continued, “During the fourth quarter we made significant progress in addressing our problem assets. Previously we had announced that two large loans were placed on non-accrual during the second quarter, resulting in our significant allowance for loan loss funding in the first half of the year. During the fourth quarter we were successful in collecting on one of these loans and we recognized a partial write-down on the other based on the appraised value and continued payment delinquency. As a result of these and other collection efforts our problem assets decreased from $17.3 million to $12.6 million.” Highlights of our financial performance are included below.

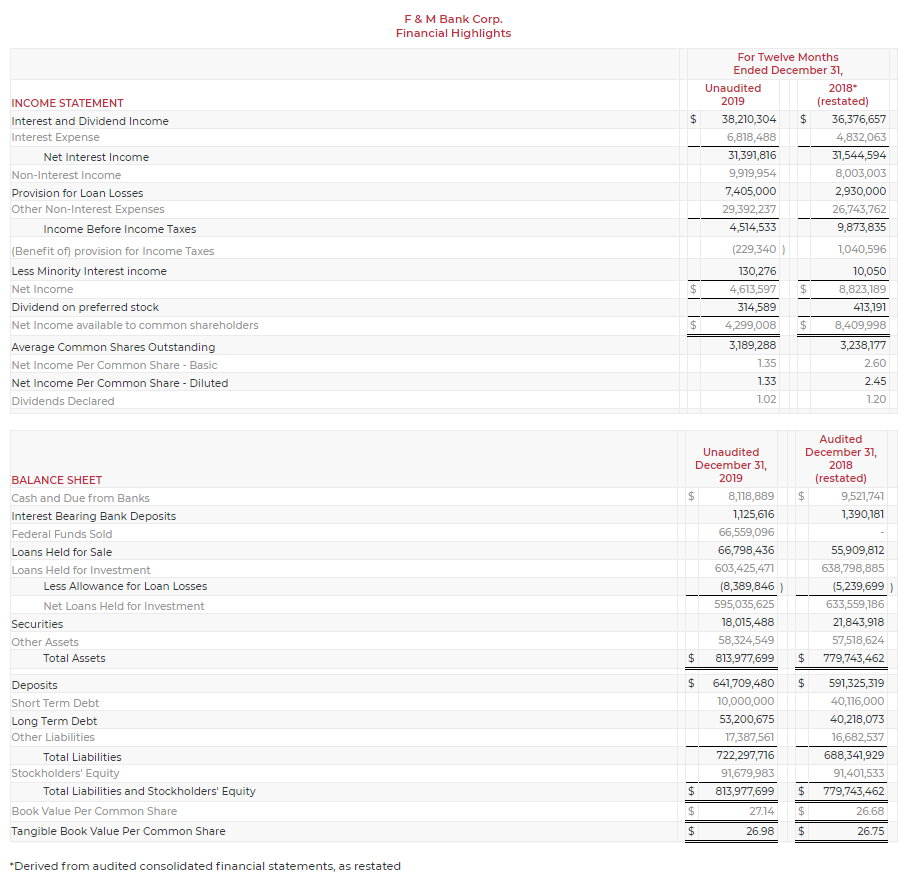

Restatement of 2018 Financial Statements: In November 2019, as a result of the sale of a portion of the Bank’s indirect dealer loan accounts, management discovered a system input error that prevented the deferred costs associated with dealer loans originated after a certain date from amortizing properly. This error in accounting resulted in a restatement of calendar year 2018 earnings of $261,728, net of tax and a correction of $248,090, net of tax for years prior to 2018 which is reflected as a reduction to retained earnings in the restated 2018 consolidated financial statements. The 2019 earnings properly reflect the amortization, which resulted in reduction of earnings of $184,890, net of tax.

F & M Bank Corp. is an independent, locally-owned, financial holding company, offering a full range of financial services, through its subsidiary, Farmers & Merchants Bank’s fourteen banking offices in Rockingham, Shenandoah, Page and Augusta Counties, Virginia. The Bank also provides additional services through a loan production office located in Penn Laird, VA and through its subsidiaries, VBS Mortgage, LLC (DBA F&M Mortgage) and VSTitle, LLC located in Harrisonburg, VA. Additional information may be found by contacting us on the internet at www.fmbankva.com or by calling (540) 896-8941.

This press release may contain “forward-looking statements” as defined by federal securities laws, which may involve significant risks and uncertainties. These statements address issues that involve risks, uncertainties, estimates and assumptions made by management, and actual results could differ materially from the results contemplated by these forward-looking statements. Factors that could have a material adverse effect on our operations and future prospects include, but are not limited to, changes in: interest rates, general economic conditions, legislative and regulatory policies, and a variety of other matters. Other risk factors are detailed from time to time in our Securities and Exchange Commission filings. Readers should consider these risks and uncertainties in evaluating forward-looking statements and should not place undue reliance on such statements. We undertake no obligation to update these statements following the date of this press release.

- The net interest margin is calculated by dividing tax equivalent net interest income by total average earning assets. Tax equivalent interest income is calculated by grossing up interest income for the amounts that are nontaxable (i.e. municipal securities and loan income) then subtracting interest expense. The tax rate utilized is 21%. The Company’s net interest margin is a common measure used by the financial service industry to determine how profitable earning assets are funded. Because the Company earns nontaxable interest income from municipal loans and securities, net interest income for the ratio is calculated on a tax equivalent basis as described above.

- The efficiency ratio is not a measurement under accounting principles generally accepted in the United States. The efficiency ratio is a common measure used by the financial services industry to determine operating efficiency. It is calculated by dividing non-interest expense by the sum of tax equivalent net interest income and non-interest income excluding gains and losses on the investment portfolio. The Company calculates this ratio in order to evaluate how efficiently it utilizes its operating structure to create income. An increase in the ratio from period to period indicates the Company is losing a greater percentage of its income to expenses.

CONTACT: Carrie Comer, EVP/Chief Financial Officer

540-896-8941 or ccomer@FMBankVA.com